Shoppers hunting for this holiday season’s hot toy, the L.O.L. Surprise, may have trouble finding it at Sears or Kmart stores. Worried about the financial health of the retail chains, the company that makes the toy, a ball that children unwrap to reveal small dolls, has reduced shipments to Sears Holdings Corp.

“We cut their credit line and shortened payment terms,” said Isaac Larian, chief executive of toy maker MGA Entertainment Inc. “If they pay one day late, we will cut them off.”

Sears once dominated American retailing and helped build famous brands, including Whirlpool appliances, Craftsman tools, Schwinn bicycles and Allstate insurance. Now, bleeding cash and losing shoppers, the 124-year-old company is scrambling to keep suppliers—the lifeblood of any retail chain—from bolting.

To guarantee shipments from LG Electronics Inc. and Samsung Electronics Co. , Sears is paying them cash up front for some goods, said people familiar with the matter. Levi Strauss & Co. has stopped supplying women’s jeans to the chain, said another person. At Clorox Co. , “We have certainly adjusted our payment terms,” said CEO Benno Dorer.

A monthslong feud between Sears and Whirlpool Corp. burst into the open last weekwhen the sides couldn’t agree on terms to keep their century-old partnership going. Earlier in 2017, Sears sued two longtime manufacturers of its Craftsman tools to keep them shipping merchandise to stores.

Reminds me of the DOT-COM days yet again...... Aivars Lode

Sprig Inc. is the latest startup casualty in the meal delivery sector.

The San Francisco company had raised more than $58 million in venture funding from firms including Greylock Partners, Social Capital, Accel Partners, Battery Ventures and others.

After growing quickly flush with venture cash, on-demand meal delivery startups have struggled to become sustainable businesses, weighed down by food and delivery costs, thin margins and fierce competition from startups as well as traditional restaurant delivery methods.

“The demand for Sprig’s convenient, high-quality food was always incredibly high, but the complexity of owning meal production through delivery at scale was a challenge,” Chief Executive Gagan Biyani said in a message to customers.

Like other on-demand services from home cleaning to laundry providers, many meal delivery startups saw rapid growth by using steeply discounted marketing offers to get people to sign up. But long-term loyalty of customers hasn’t been easy with the many different options that consumers have to choose from.

“It’s a classic venture reality,” said Ben Narasin, partner at Canvas Ventures. “I think there’s great companies doing great things here, but the category has been overfunded.”

Earlier in May, Maple Food Co. ceased operations and sold some technology to another company, Deliveroo, after raising about $26 million. Others that have shut down include SpoonRocket Inc., Dinner Lab Inc. and Kitchit Inc. In December, Berlin-based HelloFresh SE raised €85 million but at a lower share price.

Meanwhile, Munchery Inc. recently brought in a new chief executive and its two co-founders left the company amid cost cuts.

Sprig had struggled to make its model work, reorganizing last year and cutting its number of chefs. It stopped delivering to Palo Alto, Calif. to focus on San Francisco and Chicago. The company had started off with well-known chefs, but later brought in an executive who had managed airline meal production to cut costs and improve operations. Sprig’s shutdown was first reported by The Information.

A larger player in food delivery is Blue Apron Inc., which has raised $193 million and delivers meal kits for people to cook at home instead of delivering cooked meals. Despite some meal startups’ arguments to the contrary, Blue Apron’s business effectively competes against the meal providers, Mr. Narasin said. “I eat three meals day,” he said. “If Blue Apron takes one meal away, (that means) I’m not using somebody else.”

I wonder whether these will come true..... Aivars Lode

IDC Futurescape Predictions

Prediction 1: By 2017, 30% of Organizations Will Be Using Tools That Offer Automated Assistance or Assistive Technology to Support Ad Hoc Tasks Prediction 2: By 2020, 50% of Companies Will Have Consistent and Measurable Customer Experience Strategies in Place to Deliver Business Metrics to Senior Management Prediction 3: By 2017, 30% of Large Enterprise Organizations Will Be Impacted by Business Model Disruption and Will Be Forced to Make Significant Operational Changes Prediction 4: By 2020, 30% of All Purchases Will Be Made Through an Online Community Prediction 5: By 2017, Two out of Five Companies Will Invest in Workforce Optimization Initiatives to Support Employee Tool Preferences Prediction 6: By 2017, 40% of Companies Will Be Actively "Listening" to Their Employees on Social to Gauge Engagement and Improve Customer Satisfaction Prediction 7: By 2018, 15% of Organizations Will Go to Just-In-Time Project Staffing Models Tapping Talent Wherever It Is Regardless of Organizational Affiliation Prediction 8: By the End of 2018, 65% of Support Interactions Will Be Digital and Social/Community Support Will Not Be Called Out as a Separate Function Prediction 9: By the End of 2016, 50% of Companies Will Have Active Management of Communities and a Focus on Customer Advocacy in the Community

Prediction 10: By 2018, 20% of Businesses Will Rely on Business Networks for Effective Resource Management

With the ecommerce disruption this should not be a surprise..... Aivars Lode

Retail REITs have been hit by store closings, while data center landlords have fared well

Shares of real-estate investment trusts have slumped this year as a postelection sugar rush wears off.

The S&P U.S. REIT Index has fallen 1.3% so far this year. It rose 4.2% last year. Meanwhile, the S&P 500 stock index has risen 6.9% so far this year, after a 9.5% increase in 2016.

REITs have had a tough time for most the past two years as investors increasingly worried about rising interest rates, which make it more expensive for REITs to borrow.

After the election, the sector bounced higher as investors rejoiced over the prospects of a looser regulatory environment and fiscal stimulus. But the rally fizzled as investors began to worry anew about rising rates. What’s more, concerns are growing that the commercial real-estate market might have peaked, given that the sector had been a beneficiary of easy monetary policy for the past several years.

Concerns about a potential “border tax,” meanwhile, are weighing on sectors that are more exposed to trade and U.S. dollar’s strength to other currencies, such as retail and lodging REITs.

“While corporate profit growth recently turned positive again, hotel fundamentals haven’t yet seen a boost in business demand,” said Lukas Hartwich, an analyst at real-estate research firm Green Street Advisors. He noted, however, that a pickup in demand could be seen in the summer as corporate profits continue to rise. Business travel accounts for three-quarters of demand of higher quality hotels that REITs own.

To be sure, employment, inflation and wage growth in the U.S. have remained at healthy levels, supporting demand for commercial and residential real estate and keeping mortgage delinquency rates low.

And rising interest rates are usually followed by positive returns for REITs, said Brad Case, Senior Vice President of Research and Industry at the National Association of Real Estate Investment Trusts. “It’s because the macroeconomy is strengthening, conditions are improving and that’s a good thing for REITs,” he said.

Yet within REITs, the prospects of some sectors are showing signs of fading. Retail REITs have been pressured by thousands of store closings as retailers that over-expanded two decades ago suffer from the move toward online shopping.

Industrial REITs haven’t fared as well as the 31% total return the group recorded last year. Higher levels of construction activity could point to the end of an earnings boom driven by scarcity of available warehouse space.

“E-commerce sales have skyrocketed and appear to have pushed demand for warehouse space over the edge, as construction spending on warehouse assets has escalated considerably since early 2014,” said Karina Estrella, an analyst at real-estate data provider Trepp Inc.

In all, more than 200 million square feet of industrial space was delivered last year and additional supply could stunt rent and occupancy growth in the future, she said.

On the other hand, data center landlords have outperformed other real-estate investment trusts so far this year, as investors eye higher earnings from tenants beefing up their capacity to host an increasing amount of online traffic and mobile transactions from consumers.

The rising consumption of video and large businesses launching their own Internet-of-things cloud platforms are also driving demand. These data centers house servers and network equipment, and usually have leases that range from five to more than 10 years with tenants such as IBMCorp. , Oracle Corp. , Verizon CommunicationsInc.,AT&TInc., and other tech giants like Amazon.comInc. and FacebookInc. that have investment-grade credit ratings.

While construction activity is picking up pace, absorption levels, or the rate at which new supply is taken up, are healthy as demand continues to outpace supply, said Bill Stein, chief executive officer at Digital Realty Trust Inc., a San Francisco-based data center REIT, in an earnings call last month.

“Scars from the last cycle are still fresh,” Mr. Stein said.

By Esther Fung - Wall Street Journal - 23 May 2017

Lets see how this plays out with the banks.....Aivars Lode

A glut of used heavy-duty trucks means some long-haul carriers are ‘upside down’ on their rigs, owing more than the trucks are worth

A glut of used big rigs is weighing down trucking companies already mired in a prolonged slump in the freight market.

Many fleets bought scores of new trucks when transportation demand was booming a few years ago. Then U.S. manufacturing activity flagged and import growth slowed as retailers rang up disappointing sales. Freight volumes started stalling out in late 2015, leaving too many trucks competing for cargo.

Large long-haul trucking companies typically run a truck for three to five years, then trade it before the warranty expires. Repair and maintenance costs tend to skyrocket after about 500,000 miles.

Now, trucking companies are trying to trade in vehicles following one of the steepest plunges in used-truck prices since the recession. Some carriers are “upside down” on trucks in their fleets, meaning they owe more on a vehicle than it is worth.

Large carriers such as Swift Transportation Co., Knight Transportation Inc.and Werner Enterprises Inc. have said the soft market for used trucks has put a dent in their businesses, even though cargo volumes have begun to recover. Last year, some fleets wrote down the value of trucks that are many companies’ main assets.

Demand for new trucks stemmed from companies like Celadon Group Inc., an Indianapolis-based carrier that expanded its truck-leasing division from 750 vehicles under management in 2013 to 11,300 trucks in 2016.

Over the past two years, the average retail price for a used Class 8 sleeper, the heavy-duty tractor used for long-haul routes, has plunged about 22% to about $49,000 in March, according to J.D. Power Valuation Services. That translates into a decrease of some $140 million across a fleet of 10,000 trucks.

“A lot of these fleets are upside down at the time of trade. It’s forcing companies to keep their equipment longer,” said Trevor Pasmann, corporate used-truck manager at Kenworth Sales Co., a commercial-truck dealer based outside Salt Lake City.

Some carriers that expanded their fleets now are cutting the number of trucks they run. That feeds more vehicles into the market and works to keep used-truck values down.

Last month, Ryder System Inc., a commercial-truck operator with a large leasing and commercial-rental division, reported first-quarter earnings fell 32% from a year earlier. The company blamed in part the soft used-vehicle market, as well as weaker-than-expected demand for commercial-vehicle rentals.

While used-vehicle prices are showing signs of bottoming out, the supply of used big rigs is expected to remain substantial into 2020, said Chris Visser, senior commercial-truck analyst at J.D. Power. If freight demand fails to improve, he said, pricing will remain depressed.

As vehicle prices fell, some trucking companies adjusted their books to reflect lower resale values for their equipment. Carriers that were making money during the boom by trading in used vehicles found themselves ringing up smaller gains on the sale of those assets.

For many publicly traded carriers, those hits to the bottom line represented “the biggest [such] headwinds in more than 20 years,” according to a February research note from transportation analysts at Stephens Inc., an investment bank and private-equity firm.

On May 1, Celadon said it had hired Stephens as an adviser and its chief operating officer had resigned, amid an examination by the company’s audit committee of transactions involving the purchase and sale of equipment between June and December of 2016. Celadon’s auditor, BKD LLP, has withdrawn its reports for fiscal 2016, which ended June 30, and the two subsequent quarters. Celadon has been accused by two short sellers, Prescience Point Research Group and Jay Yoon, of attempting to hide mounting losses tied to its bet on the truck resale market. Celadon, through a spokesman, declined to comment.

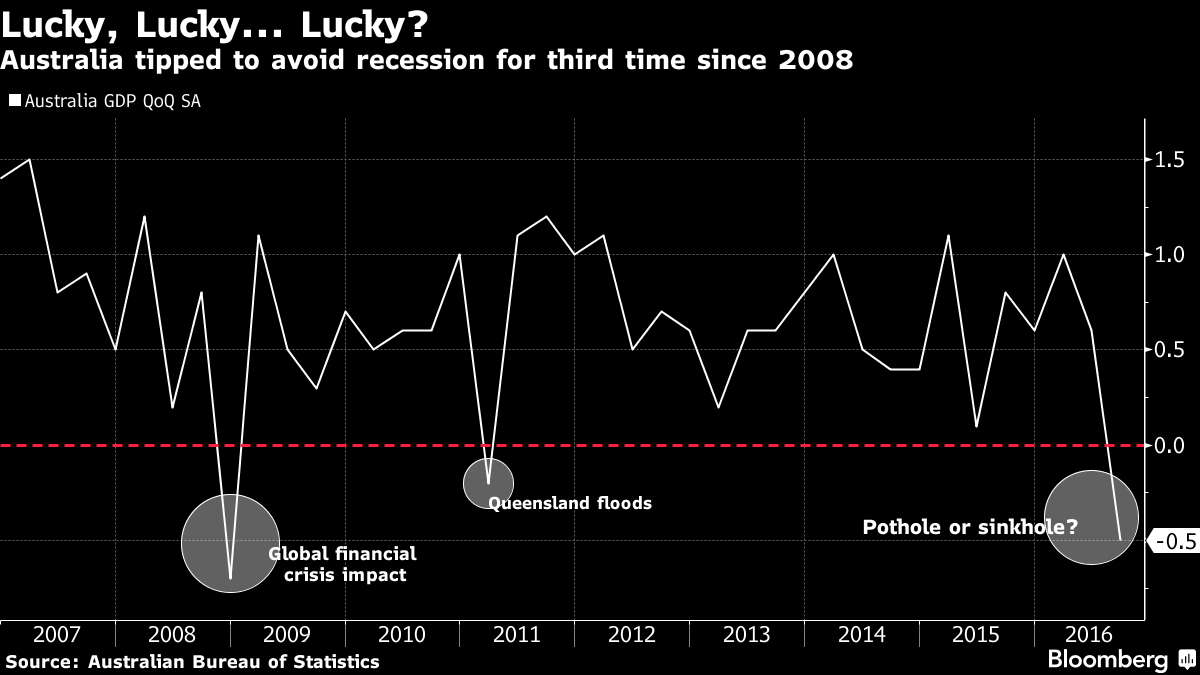

And they have rescued it for 20 years so far... Aivars Lode

The news out of Australia isn’t all gloom.

By Michael Heath

While growth figures stank last quarter, the nation is again being cushioned by its status as the developed world’s most China-dependent economy. Surging coal and iron ore prices have helped ease an erosion of national income Down Under and, together with a slower slide in mining investment, signal better prospects ahead.

Australia can thank its No. 1 trading partner, whose old economy is reviving as fiscal stimulus gets smokestacks billowing again. Traditional Chinese industries seen as proxies for growth, such as electricity and rail cargo, have collectively bounced back to the highest level in three years. The big unknown: the durability of a turnaround that’s ended a more than 50 percent drop in commodity prices between 2011 and 2016.

“This story is a big one for Australia,” said Paul Bloxham, chief Australia economist at HSBC Holdings Plc, who previously worked at the nation’s central bank. “We’ve talked about the commodity price rise as being a game-changer.”

Bloxham says the extended price slump since 2011 brought investment in new mines to a halt and as a result commodities have passed their trough. He estimates the rebound, which has seen coking coal prices rise 280 percent this year, could add about 2 percentage points to nominal gross domestic product Down Under.

Macquarie Bank Ltd. predicts Australia’s terms of trade -- export prices relative to import prices -- will climb 7 percent next year. That will help lift nominal GDP growth to more than 5 percent, which would be the best result since 2011, said James McIntyre, head of economic research in Sydney.

But this “boom” is different. While a big winner should be government revenue as higher prices boost the profits of mining companies and the taxes they pay, weaker wage growth may cancel out that benefit.

High Hopes?

Aussies probably shouldn’t bet on fatter wallets either. In the previous boom, governments recycled cash back to citizens through tax cuts, higher benefit payments and increased fiscal spending to “turbo-charge” the economy.

“That’s not going to happen this time,” said McIntyre. “Any extra revenues will help offset areas of weakness for the budget like underemployment and low wages growth; every additional dollar over that is likely to go into budget repair. Those hoping for a redux of the 2000s boom are likely to be disappointed.”

The Liberal-National coalition government is wary of incorporating higher coal and iron ore prices into its forecasts after its Labor party predecessors were burned by excessive optimism. With Australia battling to maintain its AAA credit rating and Treasurer Scott Morrison aiming to return to a balanced budget by fiscal year 2021, it could be tempting.

“We’re not forecasting it in,” Trade Minister Steven Ciobo said in an interview Thursday in Jakarta. “Treasury has made not a forecast but an assumption with respect to commodity prices. Obviously, the stronger commodity prices are, the better that that is for Australia. We’ve never pretended otherwise.”

Where the commodity spike has been showing up is in Australia’s trade balance. The monthly deficit, which blew out to A$4.2 billion ($3.1 billion) in December, has been rapidly narrowing and was just under A$1.3 billion in September.

Data out Thursday showed the deficit subsequently widened to A$1.5 billion in October, compared with economists’ forecasts for a A$610 million gap. Deutsche Bank AG analysts suggested a lag between spot and contract prices for commodities; on top of that, almost A$500 million of capital goods were imported in the month.

The deficit is still expected to narrow as the data more fully reflects coal’s surge. So Ciobo may yet oversee a trade surplus, a rarity for any minister that’s held the post.

That would prove welcome news for the government after data Wednesday showed the economy shrank in the three months through September by 0.5 percent, only the fourth quarterly contraction in the past 25 years. Economists surveyed by Bloomberg forecast an expansion this quarter of 0.6 percent.

Even if China eases stimulus, its decision to shutter excess capacity in the coal industry may continue to aid Australia, while U.S. President-elect Donald Trump’s infrastructure investment push could also provide additional support to commodities.

Exports “are a key driver of the growth story in Australia and in many respects the GDP number just reinforces the value that exports will have,” said Ciobo. “But look, it’s a volatile time. And so export growth is going to continue to be a key driver for our economy for some time.”

An Aussie who has lived around the world and done business in a large number of different countries. Aivars is an Ambassador for The Transparency Task Force, a collaborative, campaigning community dedicated to driving up the levels of transparency in financial services around the world.